How to Calculate Anti Profiteering Amount for Real Estate Developers and Builders

Recommended Read:- Why NAA Need to Revisit it’s Anti Profiteering Computation on Real Estate Companies

Anti Profiteering, as the name suggests, is a check against profiteering – something which ought to be ethical but is now a legal issue in Goods and Service Tax.

Concept

The Government wants that GST should not lead to general inflation and for this, it becomes necessary to ensure that benefits arising out of GST implementation be transferred to customers so that it may not lead to inflation. For this, anti profiteering measures will help check price rise and also put a legal obligation on businesses to pass on the benefit.

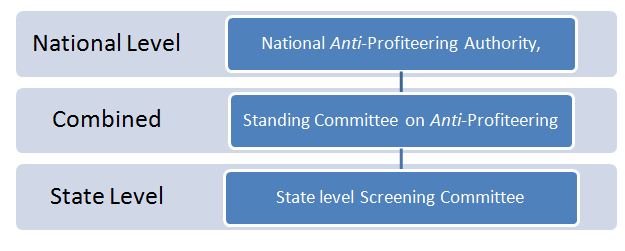

Authority for anti-profiteering regulation

The National Anti-profiteering Authority (NAA) shall be responsible for applying anti-profiteering measures in the event of a reduction in rate of GST on supply of goods or services or, if the benefit of input tax credit is not passed on to the recipients by way of commensurate reduction in prices.

Recommended Read :- How to File Complaint Under Anti Profiteering Provisions of GST

As per Rule 137 of CGST Act.2017 Sunset Clause is inserted and as per this clause Anti Profiteering authority will exist for 2 Years. What this means is that Anti Profiteering measure will remains for two years effectively form the date of constitution of Authority i.e. 22nd November 2017 to 21st November 2019

Powers of Anti Profiteering Authority

Anti Profiteering Authority shall have the followings Powers

-

Make company reduce the prices.

-

Make company refund the money to the consumer alongwith interest @ 18% p.a.

-

Order company to deposit the refund amount in the Consumer Welfare Fund (in case the buyer is not identifiable).

-

Impose monetary penalty equivalent to amount involved in undue profiteering.

-

Cancel registration of the assessee..

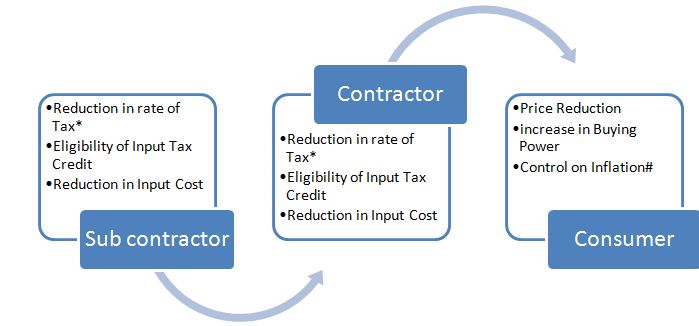

Benefits to the Builders and Customers

# It is to be extent of change in the Rate

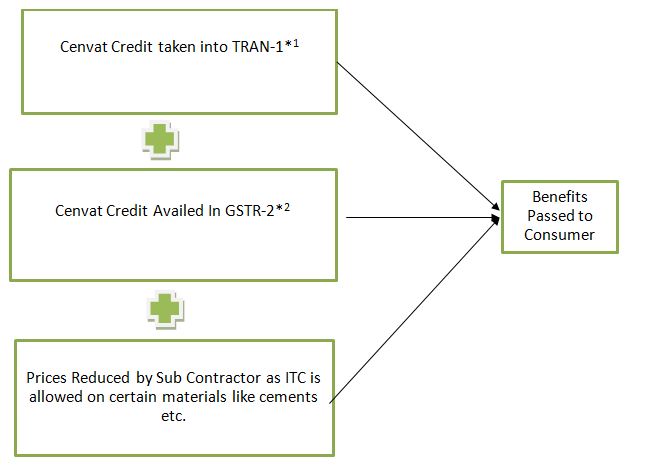

*1 There is no reduction in rate of tax in real estate developers and builders Industry

*1. Only that input tax credit which was not eligible under the previous regime but eligible under GST Regime

*2 only that amount will be considered which is in excess of previous regime Input on month to month / quarter to quarter basis.

How Benefits Are Passed on to the Customer under Anti Profiteering Clause?

-

Currently no Act or Rules provides any specified modus of operandi to pass on the benefits of anti Profiteering to the end customer, which has created a dilemma in the real Estate Industry regarding the Computation and Calculation of Anti profiteering benefits which has to be passed on to the Customers.

-

In light of no method currently prescribed by the government, Various Methods can be suggested to pass on the benefits to the customers, which can give an approximate idea to the builders and contractor while computing Anti profiteering Benefits.

-

The same Methodology should be documented and even certified by statutory auditor/ chartered Accountant for veracity purpose.

Methods with Example

-

Project by project basis

* Note- As per Rule Input tax credit claim in trans-1 is belong upto one year old stock from the date of implementation of GST i.e. 1st July,2017 provided original invoices is also withheld for claiming Input on such stock

* Note- Benefits is transfer upto first month of GST Implementation i.e. Rs/sqft

-

Computation of such benefit needs to be documented and same can be esteem by Statutory auditor or Chartered Accountant

-

In Real Estate developer/Builder there might be two type of customer

-

Running Customer- Anti profiteering Benefits may be transfer on year on year basis reduced from demand raised of last month of the year (Suggested)

-

Customers to whom possession (F&F) is given within year- Anti profiteering Benefit of his share is transferred immediately to customer at the time of F&F Settlement.

-

-

Blanket Wise

Customer Wise

{kind=link}

Disclaimer:

-

Above method is only for general understanding Of anti profiteering laws, but when it comes to reality it is very harsh process and time consuming and needs detailed analysis. The benefit transferred is through methods like one to one, bill by bill, NPR Vs NPR basis.

-

Proper computations need to be done and the same shall be duly documented. Such computation should be also certified statutory auditors/ Chartered Accountants to ensure veracity (though it is currently not a statutory obligation to obtain such certification). Such methods are all sugggestible though there is no specific method is prescribed by Govt. to calculate Anti Profiteering Benefits.

CA Ankit Gulgulia (Jain) | +91-9811653975

Related Tags Antiprofiteering, CGST, RealEstate

Admin at Charteredonline. Reach us admin@charteredonline.in