{kind=link}

- Section 3 of the Prohibition of Benami Property Transactions Act, 1988 states

that “no person shall enter into any benami transaction.”

2. What is a benami transaction?

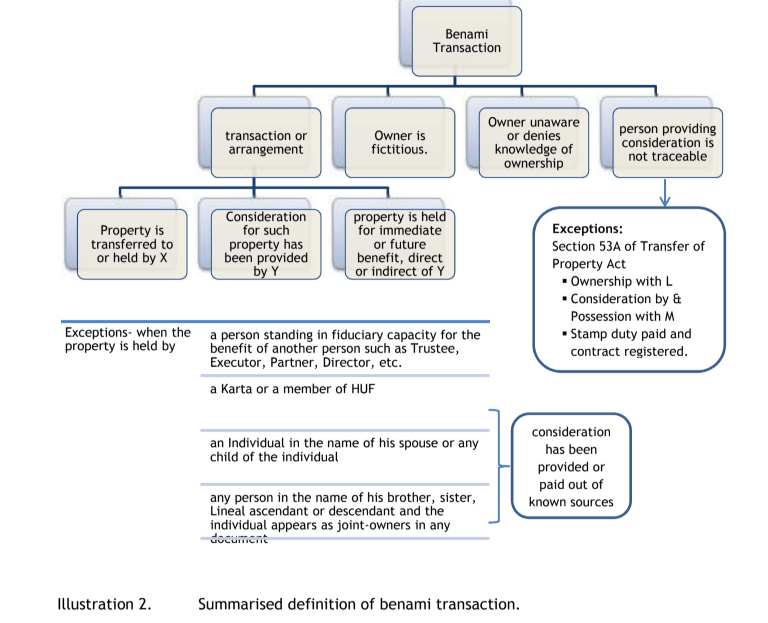

According to section 2(9), “benami transaction” means – (A) a transaction or an arrangement – (a) where a property is transferred to, or is held by, a person, and the consideration for such property has been provided, or paid by, another person; and

(b) the property is held for the immediate or future benefit, direct or indirect, of the person who has provided the consideration,

except when the property is held by –

(i) a Karta, or a member of a Hindu undivided family, as the case may be, and the property is held for his benefit or benefit of other members in the family and the consideration for such property has been paid or provided out of the known sources of

the Hindu undivided family;

(ii) a person standing in a fiduciary capacity for the benefit of another person towards whom he stands in such capacity and includes a trustee, executor, partner, director of a company, a depository or a participant as an agent of a depository under the Depositories Act, 1996, and any other person as may be notified by the Central

Government for this purpose;

(iii) any person being an individual in the name of his spouse or in the name of any child of such individual and the consideration for such property has been paid or provided out of the known sources of the individual;

(iv) any person in the name of his brother or sister or lineal ascendant or descendant, where the names of brother or sister or lineal ascendant or descendant and the individual appear as joint owners in any document, and the consideration for such property has been paid or provided out of the known sources of the individual; or

(B) a transaction or an arrangement in respect of a property carried out or made in a fictitious name.

(C) a transaction or an arrangement in respect of a property where the owner of the property is not aware of, or, denies knowledge of such ownership.

(D) a transaction or an arrangement in respect of property where the person providing the consideration is not traceable or is fictitious.

Explanation.- For the removal of doubts, it is hereby declared that benami transaction shall not include any transaction involving the allowing of possession of any property to be taken or retained in part performance of a contract referred to in section 53A of the Transfer of Property Act, 1882, if, under any law for the time being in force –

(i) consideration for such property has been provided by the person to whom possession of property has been allowed but the person who has granted possession thereof continues to hold ownership of property;

(ii) stamp duty on such transaction or arrangement has been paid; and

(iii) the contract has been registered.

3. The use of phrase “means” as distinguished from “means and includes”

signifies that the definition of “benami transaction” in the Act is exhaustive.

Exhaustive definition means that all possible items are enumerated by the

legislature in the Act and none is left for imagination.

4. The words “transaction” or “arrangement” are not defined under the Act. Blacks Law Dictionary defines the word “transaction” to mean

- Whatever may be done by one person which affects another’s rights, and out of which a cause of action may arise. (Scarborough v. Smith, 18 Kan.406.)

- “Transaction” is a broader term than “contract.” A contract is a transaction, but a transaction is not necessarily a contract. See Ter Kuile v. Marsland, 81 Ilun, 420, 31 N. Y. Supp. 5; Xenia Branch Bank v. Lee, 7 Abb. Prac. (N. Y.) 372; Roberts v. Donovan, 70 Cal. 113, 11 Pac. 599.

Blacks Law Dictionary defined the word “arrangement” to mean “When a debtor and creditor make an agreement about repayment or a debt.”

5. There are two limbs of the phrase “benami transaction” defined in Section 2(9)(A) of the Act.

5.1 The first limb of a benami transaction is the separation of vesting of ownership in the First person (also called benamidar) and the payment of consideration for such property by a Second person (also called the beneficial owner).

5.2 The second limb of a benami transaction is that the property is held for the immediate or future benefit, direct or indirect, of the previously mentioned second person (“beneficial owner”).

5.3 The terms in sub-clause (a) and (b) – first limb and second limb referred above – of section 2(9)(A) are cumulative i.e., both the conditions must be satisfied for a property to fall within the four corners of the term “benami transaction”.

6. The Act specifies four (4) exclusions from the ambit of clause (A) of the definition of “benami transaction”.

7. First exclusion

7.1 When the property is held by a Karta, or a member of a Hindu undivided family, as the case may be, and

7.2 the property is held for his benefit or benefit of other members in the family and

7.3 the consideration for such property has been paid or provided out of the known sources of the Hindu undivided family.

7.4 All the three (3) conditions are cumulative.

8. Second exclusion

8.1 When the property is held by a person standing in a fiduciary capacity for the benefit of another person towards whom he stands in such capacity and includes

(i) a trustee,

(ii) executor,

(iii) partner,

(iv) director of a company,

(v) a depository or a participant as an agent of a depository under the Depositories Act, 1996, and

(vi) any other person as may be notified by the Central Government for this purpose.

8.2 The list of persons standing in a fiduciary capacity specified in the Act is inclusive. The word “includes” when used, enlarges the meaning of the expression so defined so as to comprehend not only such things as they signify according to their natural import but also those things which the clause declares that they shall include.

8.3 The qualification – “the consideration for such property has been paid or provided out of the known sources of the” first person present in other 3 clauses of the list of exclusions is absent in this clause.

9. Third exclusion

9.1 is any person being an individual in the name of his spouse or in the name of

any child of such individual and

9.2. the consideration for such property has been paid or provided out of the known

sources of the individual.

9.3 All the two (2) conditions are cumulative.

10. Fourth exclusion

10.1 When the property is held by any person in the name of his brother or sister or lineal ascendant or descendant,

10.2 where the names of brother or sister or lineal ascendant or descendant and the

individual appear as joint owners in any document, and

10.3 the consideration for such property has been paid or provided out of the known

sources of the individual.

10.4 All the three (3) conditions are cumulative.

11. Benami transaction also includes a transaction or an arrangement in respect of a property carried out or made in a fictitious name. (Section 2(9)(B))

12. Benami transaction also includes a transaction or an arrangement in respect of a property where the owner of the property is not aware of, or, denies knowledge of such ownership. (Section 2(9)(C))

13. Benami transaction also includes a transaction or an arrangement in respect of property where the person providing the consideration is not traceable or is fictitious. (Section 2(9)(D))

14. General Exclusion of Property Transferred by Possession Deed.

Explanation to section 2(9) declares that benami transaction shall not include any transaction involving the allowing of possession of any property to be taken or retained in part performance of a contract referred to in section 53A of the Transfer of Property Act, 1882, if, under any law for the time being in force –

(iii) consideration for such property has been provided by the person to whom possession of property has been allowed but the person who has granted possession thereof continues to hold ownership of property;

(iv) stamp duty on such transaction or arrangement has been paid; and

(v) the contract has been registered.

15. Benamidar means a person or a fictitious person, as the case may be, in whose name the benami property is transferred or held and includes a person who lends his name. (Section 2(10))

16. “Beneficial owner” means a person, whether his identity is known or not, for whose benefit the benami property is held by a benamidar. (Section 2(12))

17. “Benami property” means any property which is the subject matter of benami transaction and also includes the proceeds from such property. (Section 2(8))

18. “property” means assets of any kind, whether moveable or immoveable, tangible or intangible, corporeal or incorporeal and includes any right or interest or legal documents or instruments evidencing title to or interest in the property and where the property is capable of conversion into some other form, then the property in converted form and also includes the proceeds from the property. (Section 2(28))

19. The word “transfer” includes sale, purchase or any other form of transfer of

right, title, possession or lien. (Section 2(29))

20. Judicial pronouncement on tests for determination of a benami transaction.

20.1 In the matter of Bhim Singh & Anr vs Kan Singh (And Vice Versa) 1980 AIR 727,

1980 SCR (2) 628, the Hon’ble Supreme Court of India, observed:

The principle governing the determination of the question whether a transfer is a benami transaction or not may be summed up thus:

(a) The burden of showing that a transfer is a benami transaction lies on the person who asserts that it is such a transaction;

(b) if it is proved that the purchase money came from a person other than the person in whose favour the property is transferred, the purchase is prima facie assumed to be for the benefit of the person who supplied the purchase money, unless there is evidence to the contrary;

(c) the true character of the transaction is governed by the intention of the person who has contributed the purchase money and

(d) the question as to what his intention was has to be decided on

(i) the basis of the surrounding circumstances,

(ii) the relationship of the parties,

(iii) the motives governing their action in bringing about the transaction and

(iv) their subsequent conduct etc.

All the four factors stated above may have to be considered cumulatively. (O P Sharma vs. Rajendra Prasad Shewda & Ors. (CA 8609-8610 of 2009) (SC))

20.2 In every benami transaction, the intention of the parties is the essence. The true test to determine whether the transaction is benami or not is to look to the intention of the parties viz., whether it was intended to operate as such or whether it was only meant to be colourable; if colourable, the transaction is benami, otherwise the transaction is not benami. On the other hand, if the parties intended that it should take effect, the transaction cannot be said to be benami.” (2003) 1 MLJ 823 (Madras High Court)

20.3 The Privy Council in the matter of T.P. Petherpermal Chetty vs R. Muniandy

Servai (1908) 10 BOMLR 590 Held :

A benami conveyance is not intended to be an operative instrument.

11. In Mayne’s Hindu Law (7th ed., p. 595, para. 446) the result of the authorities on the subject of benami transactions is correctly stated thus:

446…Where a transaction is once made out to be a mere benami it is evident that the benamidar absolutely disappears from the title. His name is simply an alias for

that of the person beneficially interested. The fact that A has assumed the name of B in order to cheat X can be no reason whatever why a court should assist or permit B to

cheat A. But is A requires the help pf the court to get the estate back into his own possession, or to get the title into his own name, it may be very material to consider whether A has actually cheated X or not. If he has done so by means of his alias, then it has ceased to be a mere mask, and has become a reality. It may be very proper for a court to say that it will not allow him to resume the individuality which he has once cast off in order to defraud others. If, however, he has not defrauded anyone, there can be no

reason why the court should punish his intention by giving his estate away to B, whose roguery is even more complicated than his own. This appears to be-the principle of the English decisions. For instance, persons have been allowed to recover property which they had assigned away….

…where they had intended to defraud creditors, who, in fact, were never injured….But where the fraudulent or illegal purpose has actually been effected by means of the

colourable grant, then the maxim applies, In pari delicto potior est conditio possidentis. The Court will help neither party. ‘Let estate lie where it falls.’

21. Benami transaction ~ Question of Fact or Law

21.1 The question whether the suit property in fact belongs to an individual i.e. whether he is a beneficial owner or is a benami, is a question of fact. (Narinder Singh Rao vs Avm Mahinder Singh Rao & Ors (CIVIL APPEAL NOS. 6918-6919 OF 2011) (SC))

22. Onus of proof

22.1 A Constitution Bench of the Apex Court in the judgment in SURASAIBALINI Vs.

PHANINDRA MOHAN reiterated the proposition of law as to the onus to establish the benami transaction shall lie only on the person who pleads the same.

22.2 In the matter of Valliammal (D) By LRS. v. Subramaniam and Others [(2004) 7

SCC 233], the Hon’ble Supreme Court observed :

The essence of a benami transaction is the intention of the party or parties concerned and often, such intention is shrouded in a thick veil which cannot be easily pierced through. But such difficulties do not relieve the person asserting the transaction to be benami of any part of the serious onus that rests on him, nor justify the acceptance of mere conjectures or surmises, as a substitute for proof.

22.3 In case of CIT vs. Daulat Ram Rawatmull (1 (1973) 87 ITR 349 (SC) their Lordships held :

That the onus of proving that the apparent was not the real was on the party who claimed it to be so. As it was the Department which claimed that the amount of fixed deposit receipt belonged to the respondent firm even thoughthe receipt had been issued in the name of B, the burden lay on the Department to prove that the respondent was the owner of the amount despite the fact that the receipt was in the name of B.

23. Consequences of entering into a benami transaction.

23.1 Prohibition of right to recover property held by benami.

23.1.1 No suit, claim or action to enforce any right in respect of any property held

benami against the person in whose name the property is held or against any other person shall lie by or on behalf of a person claiming to be the real owner.

23.1.2 No defence based on any right in respect of any property held benami, whether

against the person in whose name the property is held or against any other person, shall be allowed in any suit, claim or action by or on behalf of a person claiming to be the real owner of such property.

23.2 Confiscation of benami property.

23.2.1 Any property, which is the subject matter of benami transaction, shall be liable

to be confiscated by the Central Government.

23.3 Prohibition on re-transfer of property by benamidar.

23.3.1 No person, being a benamidar shall re-transfer the benami property held by him to the beneficial owner or any other person acting on his behalf.

23.3.2 Any property re-transferred in contravention of 23.3.1, the transaction of such

property shall be null and void.

23.4 Prosecution and Penalty

23.4.1 Prosecution and penalty for benami transaction prior to 1.11.2016 : Section 3(2)

23.4.2 Prosecution and penalty for benami transaction on or after 1.11.2016 : Section 53

23.4.3 Confiscation of property held benami. (Section 5)

23.4.4 Prosecution and penalty for False Information (Section 54)

CA Nirmal Ghorawat is Fellow Member at ICAI and Specializes in Benami Transaction. He is Principal Associate @ Charteredonline for Benami. You can contact him @ ‘Contact Us’ above.