lease refer to the Master Circular No. DBOD.No.BP.BC.11/21.06.001/2011-12 dated July 1, 2011 on ‘Prudential Guidelines on Capital Adequacy and Market Discipline – New Capital Adequacy Framework (NCAF)’ by which the consolidated prudential guidelines had been issued to banks on the captioned subject.

lease refer to the Master Circular No. DBOD.No.BP.BC.11/21.06.001/2011-12 dated July 1, 2011 on ‘Prudential Guidelines on Capital Adequacy and Market Discipline – New Capital Adequacy Framework (NCAF)’ by which the consolidated prudential guidelines had been issued to banks on the captioned subject.2. In terms of para 6 of the circular, four domestic credit rating agencies viz. CARE, CRISIL, FITCH India and ICRA have been accredited for the purpose of risk weighting the banks’ claims for capital adequacy purposes. The long term and short term ratings issued by the chosen domestic credit rating agencies have been mapped to the appropriate risk weights applicable as per the Standardised Approach under the Basel II Framework.

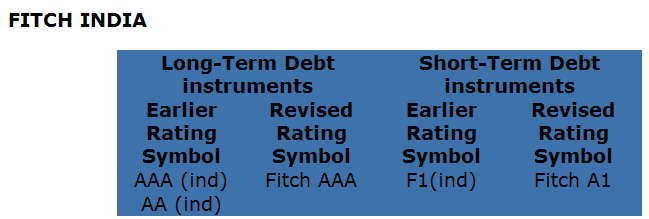

3. SEBI has, vide its circular CIR/MIRSD/4/2011 dated June 15, 2011 on ‘Standardisation of Rating Symbols and Definitions’, instructed Credit Rating Agencies (CRAs) registered with SEBI to adopt common rating symbols and rating definitions, which shall henceforth be used for the new ratings / reviews by the CRAs. Under the revised standardized system, there is no change in the long term rating symbols except that rating symbols will henceforth display the rating agency’s name as a prefix. In case of short term ratings, a rating scale denoted by ‘A’ on a scale of ‘1’ to ‘4’ (i.e. A1, A2, A3 and A4) and ‘D’ has been prescribed. The four accredited CRAs, which are registered with SEBI, have therefore revised their rating symbols of long term and short term debt instruments. The new rating symbols of the chosen CRAs vis-á-vis their old rating symbols for long term and short term instruments are furnished in Annex for ready reference.

4. The aforesaid change in rating symbols and definitions however does not effect, in any manner, the rating methodology followed by the CRAs for rating such instruments and will have no bearing on the existing ratings assigned by the CRAs under the Basel-II framework.

5. In view of above, banks are advised that they should henceforth use the revised rating symbols of the credit rating agencies with the corresponding guidance in the master circular under reference for the purpose of assigning risk weights to the various exposures.

6. All other provisions regarding external credit ratings of the master circular remain unchanged.

Source :

RBI/2011-12/217

DBOD.No.BP.BC.39 /21.06.007/2011-12

Note : As a part of Our Quality Policy , We Don’t Publish any Restricted Material on our Website . If you have issues kindly let us know here

Related Tags CreditRating, News, RBI

Admin at Charteredonline. Reach us admin@charteredonline.in