{kind=link}

GST On Transfer of Development Rights

Respected Friends,

As you all are aware that Real Estate Industry has always been an Industry prune to a lot of tax disputes and grey tax areas due to complexity of transactions and multiple state and central laws applicable simultaneously on every single transaction.

One of the several issues that has been keenly watched and studies in the Industry has been taxability on transfer of development rights (hereinafter referred to as “TDR”). In this technical paper, I intend to discuss in detail my view and supports in its favour on taxability of TDR’s in Service Tax Regime (both Positive List & Negative List) and in GST Regime w.e.f 1st July, 2017.

Introduction to Real Estate Practice – Development Rights

The Real estate sector of the country is growing at an exponential way and housing is the one of the crucial necessity of every citizen of the country. With the development in the real estate sector the most adopted model remains to be developer – land owner – customer model. There are majorly two reasons for adopting this model:-

a. The developer company itself sometimes would be capable to acquire the complete land but cannot do so due to land ceiling provisions applicable to the state. In such scenarios different group companies buy the land and pool their development rights to a single developer company.

b.In other case, on the merit that investment reduces drastically for both the developer and land owner and it is mutually beneficial situation.

The Model

The model of operation in such a scenario is as under:-

- The land owner shall acquire land on which the development is to be undertaken. The Developer enters into an agreement with land owner.

- Pursuant to this agreement, land owner transfers his ‘Development Rights’ to the developer.

- These development rights are generally transferred to the developer permanently, exclusively and on irrevocable basis.

- The consideration charged by land owner for such transfer of development rights may be in pure monetary terms or may be as a revenue share arising out of the sale proceeds of the project by the developer.

- The development rights of the land entitle the developer to enter the land, develop the land, obtain license for land conversion / development, sell the units of the projects and enter into flat buyer’s agreement with the buyers.

What are Development Rights?

Development right is fundamentally a right to develop the land for agricultural , residential or commercial use. Essentially, land like any other asset is a bundle of several rights that accrues to it. Several rights one may identify with land are development rights, possession right, cultivation right etc.

By transferring the development rights it shall not result into transfer of ownership of the land in toto but only the aspectual right to develop the land.

Taxability prior to 1st July, 2014 {Prior to Negative List Regime}

Prior to negative list regime a service was liable to service tax only if it was covered in the specified set of services on which service tax was applicable. Out of several services related to real estate industry including commercial construction, real estate agent or preferential location services the said activity of transfer of development rights finds nearest taxability contentions in ‘Renting of Immovable Property”. Whether it was taxable under this category or not follows in this discussion.

As per section 65(105)(zzzz),

Any services provided or to be provided to any person, by any other person, by renting of immovable property or any other service in relation to such renting, for use in the course of or, for furtherance of, business or commerce

“Immovable property” includes—

(i) building and part of a building, and the land appurtenant thereto;

(ii) land incidental to the use of such building or part of a building;

(iii) the common or shared areas and facilities relating thereto; and

(iv) in case of a building located in a complex or an industrial estate, all common areas and facilities relating thereto, within such complex or estate, but does not include-

a. vacant land solely used for agriculture, aquaculture, farming, forestry, animal husbandry, mining purposes

b. vacant land, whether or not having facilities clearly incidental to the use of such vacant land;

c. land used for educational, sports, circus, entertainment and parking purposes; and

d. building used solely for residential purposes and buildings used for the purposes of accommodation, including hotels, hostels, boarding houses, holiday accommodation, tents, camping facilities

(v) vacant land, given on lease or license for construction of building or temporary structure at a later stage to be used for furtherance of business or commerce;

Now, to understand the taxability of the transfer of development rights it is imperative for us to discuss that whether irrevocable transfer of development right would tantamount to lease or license of vacant land.

Lease and License

Section 105 of Transfer of Property Act, 1882 defines lease as “A lease of immovable property is a transfer of a right to enjoy such property, made for a certain time, express or implied, or in perpetuity, in consideration of a price paid or promised, or of money, a share of crops, service or any other thing of value, to be rendered periodically or on specified occasions to the transferor by the transferee, who accepts the transfer on such terms” Essentially the periodicity, perpetuity and right to enjoy such property for certain time are the main elements of a lease.

In case of Jaswantsinh Mathurasinh & anor v. Ahmedabad Municipal Corpn & ors (1992) 1 SCC 5 it was held by that “A lease creates a right or an interest in the enjoyment of demised property and a tenant or sub-tenant is entitled to remain in possession thereof until the lease is duly terminated, and eviction takes place in accordance with law.”

A license is defined in Section 52 of Indian Easements Act 1882 as ‘a right to do or continue to do, in or upon the immovable property of the grantor, something which would in the absence of such right be unlawful, such right does not amount to an easement or an interest in the property. {Muskett v. Hill (1839) 5 Bing (HC) 694 }

In Associated Hotels of India v. R N Kapoor {AIR 1959 SC 1262}, it was held that

“The following propositions may, therefore, be taken as well-established: (1) To ascertain whether a document creates a licence or lease, the substance of the document must be preferred to the form ; (2) the real test is the intention of the parties-whether they intended to create a lease or a licence; (3) if the document creates an interest in the property, it is a lease;

….

but, if it only permits another to make use of the property, of which the legal possession continues with the owner, it is a licence; and (4) if under the document a party gets exclusive possession of the property, prima facie, he is considered to be a tenant; but circumstances may be established which negative the intention to create a lease.”

In a catena of judgements including Qudraiullah v. Municipal Board Bareily (1974) 1 SCC 202 ; Rajbir Kaur v. S Chokosiri & Co. AIR 1988 SC 1845 and several others, the following principles to understand the concept of lease and license has been seen as good law :-

“There is no simple litmus test for distinguishing a lease from a license. The character of the transaction turns on the operative intent of the parties. If interest in the immovable property, entitling the transferee to its enjoyment, is created, it is a lease; If permission to use land without the right to exclusive possession is alone granted, the transaction is a license”

In MN Clubwala v. Fida Hussain Saheb AIR 1965 SC 610, it has been held that the theory of exclusive possession is a matter of considerable significance in deciding whether the transaction is a lease or a license.

Whether Transfer of Development rights is lease or license of Vacant Land

Based on above discussion, two conclusions can be carved,

a) Permanent & Irrevocable Transfer of Development Rights is not a transaction of Lease

– Lease gives revocable right to enjoy property to lessee, while in case of transfer of development rights (TDR) the right is transferred permanently and irrevocably.

Lease gives right to enjoy while TDR give right to develop.

– Lessor regains possession after lease term, while in TDR it is not the case.

Lease rights do not permit development but mere possession, while TDR permits development.

– Lease involves recurring compensation, while TDR involves fixed and generally single compensation.

b) Permanent & Irrevocable Transfer of Development Rights is not a transaction of License

– License cannot create interest in property while TDR creates interest.

– Licensee cannot transfer the product while under TDR the developers can enter in flat buyers agreement with the customers.

– Licensor discretion stands in case of license while in TDR the developer has the discretion to develop and sell the project.

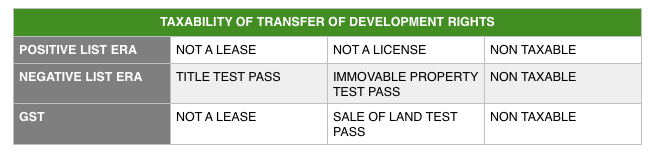

Based on above discussion, it can be inferred that this transaction of transfer (sale) of development rights is outside the purview of service tax ambit for the period prior to 1st July, 2012 and can be inferred as mere sale of right (Development right) in the immovable property.

Taxability of Transfer of Development Rights in Negative List Regime i.e. WEF 1st July, 2012

The service tax ambit was enhanced significantly with the inception of negative list regime w.e.f 1st July, 2012. Under this regime all the activities are liable to service tax except those which are outside the ambit of definition of service or are covered in negative list (section 66D) or under mega exemption notification (Not. 25/2012-ST as amended). Hence all other activities not covered above gets taxable resulting in enlarging service tax’s scope drastically.

To understand the taxability, it is imperative to understand whether the activity of transfer of development rights (TDR) would constitute a ‘service’ as per definition laid down in service tax laws.

As per section 65B(44) of Finance Act, 1994

“Service” means any activity carried out by a person for another for consideration, and includes a declared service, but shall not include—

a) an activity which constitutes ‘merely’,––

I. a ‘transfer of ‘title’ (FIRST EMPHASIS) in goods or ‘immovable property’(SECOND EMPHASIS), by way of sale, gift or in any other manner; or

II. such transfer, delivery or supply of any goods which is deemed to be a sale within the meaning of clause (29A) of Article 366 of the Constitution; or

III. a transaction in money or actionable claim;

b) a provision of service by an employee to the employer in the course of or in relation to his employment;

c) Fees taken in any Court or tribunal established under any law for the time being in force.

CBEC – Education Guide (Dated 20.6.2012) – Extracts

2.6 Activity to be taxable should not constitute only a transfer in title of goods or immovable property by way of sale, gift or in any other manner

♦Mere transfer of title in goods or immovable property by way of sale, gift or in any other manner for a consideration does not constitute service.

…

♦Immovable property has not been defined in the Act. Therefore the definition of immovable property in the General Clauses Act, 1897 will be applicable which defines immovable property to include land, benefits to arise out of land, and things attached to the earth, or permanently fastened to anything attached to the earth.

2.6.1 What is the significance of the phrase ‘transfer of title’?

Transfer of title’ means change in ownership. Mere transfer of custody or possession over goods or immovable property where ownership is not transferred does not amount to transfer of title. For example giving the property on rent or goods for use on hire would not involve a transfer of title.

The Concept of ‘Title in Immovable Property’

In Canbank Financial Services v. Custodian, 2004 (8) SCC 355 = 2004 (7) SC 507, it was held by the apex court that the word ‘Title’ generally used in the context to the property means a right in the property. Title in a property connotes a bundle of rights. Subject to prohibitory or regulatory statute, such rights are capable of being transferred. The ‘Title’ in an immovable property is the means whereby a person’s right to such property in presenti is established and does not include a bare expectancy to get such right in due course of time.

‘Title’ is a broad expression in law, which need not be always understood as akin to ownership. The said expression conveys different forms of a right to a property which can include right to possess such property. In case of Rajendra Kumar v. Poosamal { AIR 1975 Mad. 379} the Hon’ble Madras HC has laid that ‘Title’ means a present right or interest in an immovable property capable of contracting to convey and cannot be understood as something equivalent to the process of making of title.

In Syndicate Bank v. Estate Officer { AIR 2007 SC 3169 }, it was held by Supreme Court that :-

“A jurisprudential title to a property may not be a title of an owner. A title which is subordinate to an owner and which need not be created by reason of a registered deed of conveyance may at times create title. The title which is created in a person may be a limited one, although conferment of full title may be governed upon fulfilment of certain conditions. Whether all such conditions have been fulfilled or not would essentially be a question of fact in each case. “

In Union of India v. Vasavi Co-operative Housing Society { 2002 (5) ALD 532 – AP }

100. The word ‘Title’ includes a right, but is the more general word. ‘Every right is a title though every title is not such a right’ for which an action lies. Blackstone defines it to be “The means whereby the owner of lands has the just possession of his property.“”TITLE” is the means whereby a person’s right to property is established. (See: P.Ramanatha Aiyar’s the Law Lexicon – 1997 Edition).

From above discussion, one may hold a view that the word ‘title’ does not necessarily infer to the ownership but to the right(s) vested in the property as held by the courts in catena of judgements as mentioned above. Further land as discussed previously is a bundle of rights.

A right transferred by way of sale is a Title transferred by way of sale. Further on the theory discussed, it can be a view taken that the activity of permanent and irrevocable sale of development right is a mere transfer of title of immovable property by way of sale and hence shall be outside the purview of service tax even in the negative list regime.

Immovable property – The Concept

The term ‘immovable property’ has not been defined under GST law. The General Clauses Act, 1987 defines “immovable property” as to include land, benefits to arise out of land, and things attached to the earth, or permanently fastened to anything attached to the earth. Section 2(6) of the Registration Act, 1908 defines “immovable property” to include land, buildings, hereditary allowances, rights to ways, lights, ferries, fisheries or any other benefit to arise out of land, and things attached to the earth or permanently fastened to anything which is attached to the earth, but not standing timber, growing crops nor grass

Other Benefits Arising out of Land is as Good As Immovable Property

As per Section 3(4) of Bombay Land Revenue Code, 1879 ‘land’ includes benefits to arise out of land and things attached to the earth or permanently fastened to anything attached to the earth and also shares in or charges on the revenue or rent of village or other defined portions of territory.

In the case of Safiya Bee vs Mohd. Vajahath Hussain – (2011) 2 SCC 94, the Apex court held that ‘land’ includes rights in or over land, benefits to arise out of land. The Apex court in the case of Pradeep Oil Corporation vs Municipal Corporation of Delhi – (2011) 5 SCC 270 observed that land includes benefits to arise out of land

a. Lake is an immovable property and therefore the petitioner’s right to enter in that estate, which he does not own and take away fish from the lake is a ‘Profit a Prendre’ and in India it is regarded as a benefit to arise out of the land and hence it is immovable property. – Anand Behera v. State of Orissa (1955) 2 SCR 919.

b. Felling, cutting and removing bamboos from forest for the manufacture of paper is a benefit to arise out of land and hence it would be an interest in immovable property. – State of Orissa v. Titagarh Paper Mills Company Limited AIR 1985 SC 1293. Right to enter upon land and cut trees is a benefit arising out of land – Shantabai V. State of Bombay AIR 1958 SC 532.

c. Congregation of buyers and sellers is enough to constitute a bazaar and the right to hold a bazaar is an interest in the land – Bibi Sayeeda v. State of Bihar (1996) 9 SCC 516. Further, Hon’ble Mumbai High Court in a case of Chhada Housing Development Corporation v. Bibijan Shaikh Farid reported in 2007 (3) Mah. L.J.P. 402 lay down that “the expression TDR, is transfer of development rights, which enables the FSI to be used on any other plot of land generated from some other plot and can be used in terms of DC Regulations in force. It is the benefit arising out of land and is immovable property.

On an understanding of the law laid down by various Courts, of the term ‘immovable property, it can be safely stated that TDR’s are the benefits arising out of the land and the same is an immovable property.

By Jointly reading above, It can be carved a view that Transfer of TDR on Permanent basis is transfer of “Title” in “Immovable Property” and shall be outside the Ambit of Service Tax in Negative List.

Taxability of TDR Under GST Regime

1.As per Section 9 of the Central Goods and Service Tax Act, 2017 (CGST Act), Central GST shall be levied on all intra-state supply of goods or services or both. Section 2(52) of the CGST Act defines the term ‘goods’ as “every kind of moveable property other than…..”. Further, ‘service’ as defined under Section 2(102) of the CGST Act covers “anything other than goods,…………..

We have already discussed above the judgements in context to Title & Immovable Property that still holds good in GST Regime. The aspect that needs discussion is the specific changes GST Law has brought in terms of taxability of Such Land Related Transactions.

Hence, it would be interesting to note that Schedule III to the CGST Act contains a negative list, enlisting activities which shall neither be treated as supply of goods nor supply of services.

Paragraph 5 of Schedule III covers ‘sale of land and, subject to clause (b) of paragraph 5 of Schedule II, sale of building’.

Paragraph 6 covers Actionable claims, other than lottery, betting and gambling.

At this juncture, it shall be important to understand whether the grant of development right and subsequent transfer of interest in land by land owner amounts to sale of land or not? It may be noted that the expressions ‘land’ or ‘sale of land’ has not been defined under the GST Law

a.Let us first analyse the word ‘sale’. As per Section 54 of Transfer of Property Act, 1882, ‘’sale’ is a transfer of ownership in exchange for a price paid or promised or part- paid and part-promised. Hon’ble Bombay High Court in the case of Provident investment Co. Ltd vs Commissioner of income tax – AIR 1954 Bom 95 observed that a sale or transfer presupposes the existence of the property which is sold or transferred. It presupposes the transfer from one person to another of the right in the property.

b.Hon’ble Guwahati High Court in the case of Nagen Hazarika vs Manorama Sharma – AIR 2007 Gau 62 held that the expression ‘title’ is a broad expression in law which cannot always be understood as akin to ownership. It conveys different forms of a right to a property which can include right to possess such property

C.As per Aiyar’s Law Dictionary, the expression ‘title’ in the general proposition means that, when equities are equal that he has the legal title will be preferred, includes in its broadest sense all rights capable of being enjoyed and secured under the law. One holding a legal title of lands is certainly included but rights amounting to less than the full legal title are equally included with it. Title to land is the evidence of his right or the extent of his interest

d.The apex Court in the case of Sunil Siddhartha Bhai v. CIT – AIR 1986 SC 368 observed that in its general sense, the expression ‘transfer of property’ connotes passing of the entire bundle of rights from the transferor to the transferee. In another case, the transfer may consist of one of the estates only, out of all may be a reduction of the exclusive interest in the totality of rights of the original property is a larger interest than a share in that property. To the extent to which exclusive interest is reduced to a shared interest it would seem that there is transfer of interest

E Syndicate Bank vs Estate Officer – AIR 2007 SC 3169, the Supreme Court held that a jurisprudential title to a property may not be title of an owner. A title which is subordinate to an owner and which need not be created by reason of a registered deed of conveyance may at times create title. The title which is created in a person may be a limited one, although conferment of full title may be governed upon fulfilment of certain conditions. Whether all such conditions have been fulfilled or not would essentially be a question of fact in each case

On an understanding of the above judgements, we can infer that the word ‘sale’ denotes transfer of title which is irrevocable and permanent. Hence ‘sale of land’ denotes ‘transfer of title in land. HENCE SALE OF LAND (GST REGIME) STATUS QUO TRANSFER OF TITLE (NEGATIVE LIST)

Hence, in our view the the taxability of TDR is as summed up under:-

To the contrary, CBEC conferred by section 148 vide Notification No. 4/2018 – Central Tax (Rate) dated 25.01.2018 has notified that a registered persons who supplies development rights to a developer, builder, construction company etc. against consideration, wholly or partly, in the form of construction service of complex, building or civil structure shall be regarded as a class of person in whose case the liability to pay central tax on supply of the said services shall arise and accordingly and the tax shall be paid at the time when the said developer, builder, construction company or any other registered person, as the case may be, transfers possession or the right in the constructed complex, building or civil structure, to the person supplying the development rights by entering into a conveyance deed or similar instrument (for example allotment letter). However, it is important to note that the above notification does not, and cannot create a charge on something that is not taxable within the purview of the charging section of the Act and the constitutional segregation of law making powers which as per above discussion is not liable for GST.

Also, In the Negative List Regime, it is learnt the DGCEI has issued SCN’s to several assesses on this matter.

Before Partying…

Hence, since GST is a new law and its interpretations are still developing. Until settled principles emerge by way of judicial precedents and more clarity is arrived at on the above discussed issues one may decide to:

a.Either take a conservative approach by paying GST on TDR’s; or

b.Pay GST under protest and make an application seeking refund (subject to the principle of

unjust enrichment); or

c.Seek an Advance Ruling in all States, and if such a ruling goes in favour of revenue, then

move the Appellate Authorities / Courts for redressal of such grievance.

It appears that this vexed issue will settle only with the intervention of Courts or the Government.

Disclaimer :- This Article is for educational Purpose only

Related Tags CA Ankit Gulgulia, CGST, GST

FCA, CWM (AAFM-US), CBV, CIFRS, R-ID, B.COM (H), RV* (IBBI)

Practising Chartered Accountant in Netaji Subhash Place, New Delhi. He is well connected business oriented professional with specialisation in Taxation (Direct & Indirect) and Corporate Laws and an enriching experience of more than 15 years. He can be contacted ankitgulgulia@gmail.com.